There is a lot of talk about “tax strategies” for highly appreciated stock (including from yours truly 😎).

There is a good reason why — there are a lot of meaningful ways to reduce taxes and increase your net worth. It’s FAR easier to reduce your taxes than have an investment portfolio outperform the market.

BUT….a surprising amount of tax strategies are quietly—or sometimes aggressively—conflating tax deferral with tax elimination.

That distinction matters. A lot.

Don’t get me wrong—deferring a tax can be powerful. Like 2% per year of extra after-tax return powerful.

But it is NOT an elimination of the tax. And thinking you eliminated a tax that is still very much coming is how people make costly decisions with concentrated stock.

So in this publication of The Equity Advantage, we dive in to help you:

Know what your tax strategy is actually doing: Eliminate, Reduce, or Defer.

Help quantify the real economic impact of each approach—so you can decide when complexity is justified and when it isn’t.

IMPORTANT FLAG: We always encourage clients to prioritize (1) their financial goals/plan, then (2) their investment portfolio and risk tolerance, with (3) tax strategy as the last focus. That isn’t to trivialize tax strategy—it can be very powerful! But rather, to ensure that you don’t allow a potential tax savings to misalign your investment/risk or financial plan (proverbial “tail wagging the dog”).

The Three Buckets: Eliminate, Reduce, Defer

The tax strategies for appreciated stock fall into one of three buckets. It can admittedly be a bit opaque because there is the potential for amplified savings when you combine strategies across buckets (e.g. defer taxes, which allow you to reduce the rate you pay when you sell). But it’s important to understand what each strategy within the three groups do, so that you can chart your overall plan for what is going to work best for you.

1. ELIMINATE the Tax (Rare, Powerful, Limited)

There are only a handful of ways to never pay capital gains tax on appreciated stock.

QSBS (Qualified Small Business Stock)

QSBS is amazing, IF you quality. By and large, QSBS would allow most individuals to eliminate 50-100% of federal capital gains up (subject to limits), as well as also eliminate tax at the state level for many (but not all) states. Pretty damn awesome!

But here’s the rub—achieving QSBS is highly technical and specific (must meet each of a large number of criteria). This makes it an extremely narrow use case, applicable to a tiny fraction of assets. 99%+ of appreciated stock will not qualify.

Donate the Stock

Donating appreciated stock to charity eliminates capital gains tax on that asset, and you get a tax deduction for full amount donated (subject to limits).

It’s a powerful way to amplify the value of your giving if you are charitably inclined. For folks who are, we utilize this strategy frequently.

But if you are not charitably inclined (which is perfectly OK), giving away stock is going to reduced your net worth (no surprise there).

Step-Up in Basis at Death

When you die, assets held in your estate generally receive a step-up in cost basis (i.e. the price the stock was purchased at is changed to the current value). Capital gains tax disappears. This is real. And it’s powerful.

It’s also not a planning strategy so much as an estate planning outcome—and not exactly a goal anyone is rushing toward.

0% Long-Term Capital Gains Bracket

Federally, a 0% LTCG bracket exists. Which in theory means it is possible to sell appreciated stock and pay no federal capital gains tax.

But in practice:

Most high-earning professionals have income every year. RSUs, NSOs, W-2 wages, interest, dividends, and consulting income push you out of this bracket quickly

And even in retirement, stock dividends, social security income and 401k distributions frequently eat up most/all of this window

This is not to say it cant work; it does work in very specific situations/years, such as sabbaticals, career gaps, and early retirement.

But it’s uncommon, and the 0% window is not that large — making the strategy have limited applicable use cases.

2. REDUCE the Tax: Where Most Value Is Actually Created

If elimination is rare, reduction and deferral are where most real-world planning happens.

These strategies don’t avoid taxes entirely—but they can dramatically lower what you pay.

Reduce Total Capital Gains (Lot Management)

Which shares you sell matters. Smart lot selection can:

Reduce total realized gains

Smooth taxable income across years

Create flexibility when paired with other planning

This may sound boring, and honestly it kind of is. But…it’s also one of the most consistently valuable tax tools we use.

Pay a Lower Long-Term Capital Gains (LTCG) Rate

Federal LTCG rates are progressive like most federal taxes, so they step up meaningfully as income/gains increase, going from 0% —> 15% —> 18.8% (15% LTCG + 3.8% NIIT) —> (15% LTCG + 3.8% NIIT).

Crossing thresholds unintentionally can cost hundreds of thousands of dollars over time.

Bracket-aware selling—especially when combined with equity comp income—is often overlooked and frequently mismanaged.

Reduce or Eliminate State Capital Gains Tax

State taxes are real. And in some situations (namely CA, NY and WA), can be quite painful.

Two broad approaches:

Multi-year state bracket management. Most state tax brackets are progressive. By spreading a capital gain over multiple years, the marginal rate the gain is taxed at declines.

Relocation planning. If you desire to, or plan on, relocating to a lower- or no-tax state in the next handful of years, then waiting to sell when you live in your new state will lower your overall tax burden.

3. DEFER Paying the Tax: Powerful—but Still a Bill

Now let’s talk about the most misunderstood category: tax deferal.

Deferral does not mean elimination. It means:

You don’t pay taxestoday

You still owe them eventually

That doesn’t make deferral bad. Quite the opposite—deferral strategies are frequently very beneficial.

But they are frequently marketed as tax “savings”, and that’s kind of BS.

If I buy a $1000 item during a 10% off sale, I paid $900 and truly saved $100. I have it my pocket to do whatever I please with.

But if I sell a stock and would owe $100 of capital gains — I don’t save the $100 if I sell on January 1st 2026 instead of December 31st 2025. I still owe the $100, I just get an additional year until I have to pay the government.

If deferring sounds underwhelming, I’d disagree. It can be a powerful tool to add significant after-tax wealth, predominately from two sources:

Investment gains on deferred taxes. Every dollar of tax you defer/don't pay this year has the ability to earn incremental financial returns. How much benefit that provides you depends on a handful of factors, but many times it can deliver2-5% per year in additional after-tax wealth.

Combine with tax reduction (defer to a future year when you will pay less tax). If relocation to a lower-tax-state, a sabbatical, starting a company, early retirement — or lower income year(s) for any reason are in your future — then in addition to generating gains on the deferred taxes each year, you can also likely amplify the benefit by eventually paying a lower tax rate when you do sell.

Common Tax-Deferral Strategies for Concentrated Stock

Below are some of the most common tax-deferral strategies we evaluate for clients with highly appreciated, concentrated stock. Each can be useful in the right situation—but none should be confused with permanently eliminating taxes.

Tax-Loss Harvesting (Including Tax-Aware Long/Short Strategies)

Tax-loss harvesting uses realized investment losses to offset realized capital gains.

In more advanced implementations—such as direct indexing or tax-aware long/short strategies (e.g. 130/30)—losses can be generated more consistently, allowing for ongoing offset of gains while maintaining market exposure.

All in, it's a good tool to help you (1) diversify out of a concentrated position, and (2) defer some of the capital gains tax (how much depends on many factors).

Exchange Funds

Exchange funds allow multiple investors to contribute concentrated stock into a pooled vehicle and receive a diversified basket of stocks in return—without triggering an immediate taxable sale.

The key tradeoff:

You gain diversification today

You retain a deferred embedded tax liability

They have limitations; most notably a time commitment of 7 years. But after that you get a diversified portfolio of stocks back to you. And you (1) diversified out of a concentrated position, and (2) deferred the capital gains tax for many years

Section 351 Exchanges

A 351 exchange involves contributing a diversified portfolio of stocks into a newly formed Exchange-Traded Fund (ETF), and receiving back shares of the newly created ETF (of the same dollar amount and tax basis as all the stock you contributed).

Charitable Remainder Trusts (CRUT / CRAT)

A charitable remainder trust allows you to contribute appreciated stock into a trust you create, sell it once in the trust without being taxed initially, and receive distributions back to yourself over time.

There are multiple nuances and costs associated with CRTs. But mechanically:

Capital gains tax is deferred until you distribute them from the CRT back to you

You choose the distribution schedule back to you (typically between 2-20 years)

Some assets must pass to charity

CRTs can be extremely effective when charitable intent already exists, as it allows one to meet two main goals: (1) give to charity, and (2) diversify without immediate recognition of capital gains.

Opportunity Zone Investments

Opportunity Zones (OZ) allow capital gains to be reinvested into qualifying projects, deferring tax until a future date, and potentially reducing taxes on both (i) the recognized gain and (ii) the new appreciation of the OZ investment. Key considerations and flags are:

OZ funds are a bit unique in that you invest after a sale occurs (contrary to many other strategies that require action prior to the sale)

OZ funds are long-term, illiquid, and typically have higher fees

Benefits depend heavily on project quality and time horizon

These can work well in specific cases, but they are investment decisions first, tax strategies second.

Quantifying the Impact for Deferrals

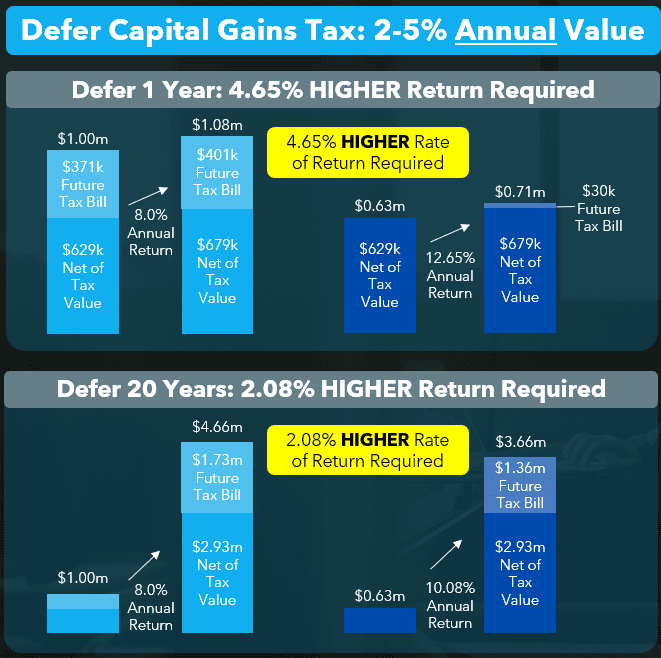

I’m a numbers geek, so lets attempt to quantify the potential value of a deferral. High level, deferring capital gains can be worth ~2–5% per year in after-tax wealth (what you really care about). Let’s talk it through (with visual support below)

Let’s say you have an investment you bought for practically $0 that is now worth $1m. You live in California, and are at the top tax bracket

Option 1: If you were able to use a deferral strategy to NOT sell today (but still diversify into something similar to the SP500; assume an 8% return), and then sell in 10 years (and pay the tax then)—you’d have $2.93m after tax

Option 2: If you instead sold today (to diversify), and paid the tax today, you’d have $0.63m. If that was invested for 10 years, and then sold, you’d need a 10.08% annual return — more than 2% higher— to have the same $2.93m after tax

The Right Way to Evaluate Tax Strategies

If your main focus when considering tax strategies is “How do I pay no tax?” then you’re thinking about this the wrong way—because that’s rare. Instead, your goal should be to understand exactly what your tax strategy is doing, and what its short-term and long-term benefits are.

Every time we evaluate a strategy for a client, we force clarity on:

Eliminate vs. reduce vs. defer

Magnitude of benefit

Tradeoffs, complexity, and loss of flexibility

Alignment with career, concentration risk, and life plans

Final Thought

Tax strategy is powerful, but it needs to be tactical, intentional, and considered in conjunction with your goals, product fees, time commitments and constraints. Many times saving taxes makes sense. Other times it doesn't.

And whenever you assess, always keep in mind:

Deferral is most common, and can add 2% or more per year in some situations

Reduction is often underutilized, but tools exist (especially across multiple years), and it can pair well with deferral to amplify savings

Elimination is best, but quite rare, and should be treated as such

If you’re sitting on highly appreciated stock, you’ve got lots of ways to approach the problem. Doing so with a plan is almost always better than proceeding without one. Or worse, thinking you solved a (tax) problem that’s still waiting for you later.