Let's say you've done something right. You joined a company early, got a meaningful equity grant, held on through the volatility, and now 7, even 8 figures of wealth (a large chunk of your net worth) is sitting in a single stock.

Congratulations! Also: now what?

It's a huge win, and put your personal finances in a great spot. But....how you diversify (assuming you want to; that's a separate topic) in a tax-smart way is a new challenge to navigate. And a surprisingly easy one to mess up.

The mistake I see most often isn't making a decision too quickly; it's the opposite. Defaulting to inaction because they either (i) don't know what to do, or (ii) are so afraid of overpaying on taxes that they don't do anything at all.

And that puts aside confusing tax deferral with tax elimination (I wrote a whole article about that — it's one of the more expensive mix-ups in financial planning).

This article lays out the tax-smart diversification toolkit I use with my clients. Five strategies, evaluated across six dimensions. No one strategy is more "right" than the other. It's about understanding the trade-offs that come with each, in order to choose the strategy (or combination of strategies) that is best for you.

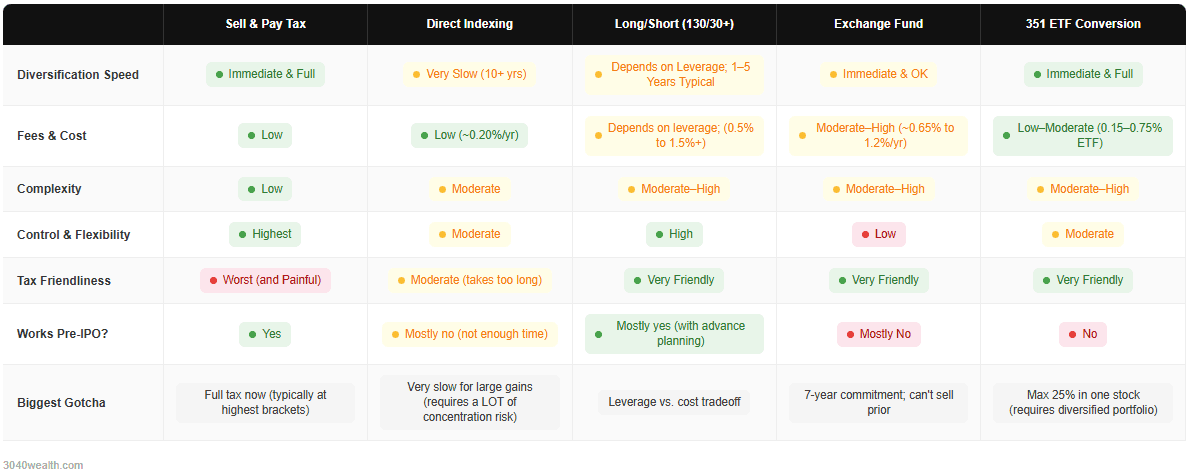

TL;DR Cheatsheet Table

If you dont want the details, the image below provides a rapid summary of the key plus/minuses:

A Note on Public vs. Private Stock

Most of these strategies assume you own publicly traded stock. A few of these can work for pre-IPO/private company shares too, but the availability narrows significantly. I flag this for each strategy, because if you're a SpaceX, Anthropic, OpenAI, Stripe, or Databricks employee reading this ahead of a liquidity event, the pre/post-IPO distinction matters a lot for what's available to you right now vs. what opens up later.

The Six Dimensions I'll Grade Each Strategy On

Before diving in, here are the six vectors worth evaluating for any exit strategy:

Diversification Speed & Completeness. How fast and how fully does it get you out of the concentrated position?

Fees & Cost. What does it actually cost to execute and maintain?

Complexity. How hard is it to do, and how many moving parts does it involve?

Control, Flexibility & Customization. How much do you stay in charge of the process?

Tax Friendliness. Does it reduce, defer, or eliminate taxes — and how meaningfully?

Key Limitations & Constraints. What are the real gotchas?

Now let's go through each strategy.

Strategy 1: Sell It and Pay the Tax

The baseline. The simplest answer. It's tax-painful, but that's the only tradeoff.

You sell your shares. You pay capital gains tax. You reinvest in a diversified portfolio. Done.

Diversification speed & completeness: Immediate and complete. You can be fully diversified the same day you sell, or you can stage the sales over 2–4 years to spread the tax hit and potentially lower your marginal rate. Either way, this is the fastest path to being fully out.

Fees & cost: Low. There's no strategy layer on top of this — no fund fee, no partnership structure. The "cost" is the immediate triggering of capital gains tax. But that figure can be considerable (up to 23.8% federal + up to 13.3% for some states).

Complexity: Low(ish). Deciding on your selling strategy is a major focus (how much you sell and when). That's separate from this article. But that aside, this is operationally simple.

Control, flexibility & customization: The highest of any strategy. You decide when to sell, which lots to prioritize, when to stop, when to accelerate.

Tax friendliness: The least friendly option in the toolkit — you're recognizing the full gain, typically at the highest brackets.

Key limitations: There's no mechanism to defer or reduce the gain beyond timing.

Works for private stock? Yes (presuming you're being offered the ability to sell in a tender).

The honest take: If your gain isn't enormous relative to your portfolio, or you're in a lower-tax state, or if you want to be done and move on — just sell it. The complexity premium for other strategies is real, and you should make sure it clears the bar before you pay it.

Strategy 2: Direct Indexing (Tax-Loss Harvesting, But Slow)

The most accessible tax-deferral strategy — but often misunderstood as something that can fully solve a large concentrated position on its own.

Direct indexing builds an index-like portfolio of individual stocks. Some go up more than others, and when a stock declines (e.g. Pepsi) it sells it and reinvests the cash in a similar company (e.g. Coca Cola). Those realized capital losses can be used to offset realized capital gains from your concentrated company stock. But it's slow....really slow.

Diversification speed & completeness: Slow; very slow for large positions. We're typically talking 10+ years to make a big dent in a meaningful concentrated position (and most of the benefit comes in the first couple years). Said another way, this will not diversify you; you continue to take a lot of company stock risk

Fees & cost: Low to moderate. Most platforms charge around 0.20% annually. There's no lockup, no complexity premium, and losses generated are a real financial asset.

Complexity: Moderate in concept, but mostly low in practice — the platform handles the harvesting logic algorithmically. Your advisor manages exclusions (so you're not buying back your concentrated stock during the transition), customizations, and the overall pace.

Control, flexibility & customization: Moderate. You can exclude individual stocks or sectors and pause or adjust at any point, and the direct index portion of the portfolio remains fully liquid throughout.

Tax friendliness: Moderate — and the honest caveat is that "takes too long" is a real limitation for most people with large concentrated positions. Works best as part of a broader strategy, not a standalone solution.

Key limitations: The gradualism is the point — and also the problem. If your company stock position is massive relative to your other assets, the loss harvesting capacity from Direct Indexing will not be close to enough of what you need, which means you're carrying single-stock risk throughout the transition (which is by far the bigger problem we recommend clients solve vs paying lower taxes).

Works for private stock? Mostly no. Tax loss harvesting does work to offset private company gains. But there's usually not enough time to generate meaningful losses in a given year to offset much.

Strategy 3: Tax-Aware Long/Short (130/30 and Beyond)

The turbocharged version of direct indexing. Much more powerful and genuinely compelling for large concentrated positions.

A long/short strategy maintains your target market exposure (say, 100% of your investable assets in equities), but adds a long sleeve and a short sleeve on top. A 130/30 portfolio goes 130% long and 30% short, netting to 100% market exposure — but with roughly 60% more positions generating harvesting opportunities. And you can increase the leverage ratio materially higher (up to 250/150 for example) to generate more losses sooner if need be.

It works so much better than Direct Indexing because there are a lot more positions, and you are both long and short, meaning a lot more individual stocks can lose value in any given environment (which you sell for the capital loss benefit) — while the overall portfolio continues to track the index you chose (i.e. SP500).

I covered this in depth in a recent SpaceX tender article, but the simplified version: in the right scenario, a 200/100 allocation on a $3M portfolio can generate enough losses to offset a $1M+ capital gain in the same year. That's not marketing — that's math.

Diversification speed & completeness: Can be very quick and substantial, depending on the leverage ratio and how aggressively you sell. Full diversification in 1–5 years is possible, and with careful planning a large portion (e.g. 50-75%) of diversification can be immediately had.

Fees & cost: Moderate to high. Two fees exist: (i) manager fee and (ii) financing costs (since you are borrowing). Depending on the leverage ratio, total costs can run from 0.5% to 1.5%+ annually. Many times it's more than justified given the tax alpha (can be 2.5%-plus per year); but you should run the math.

Complexity: Moderate to high. Requires a margin-enabled account, manager selection, leverage ratio decisions, and ongoing monitoring. The leverage ratio (115/15 up to 250/250) is a meaningful variable with different risk and tax trade-offs at each level. Not available at all custodians or in tax-advantaged accounts.

Control, flexibility & customization: High on the concentrated stock side. You control the pace of selling, the leverage ratio, the target index, any exclusions, etc.

Tax friendliness: Extremely friendly for large positions. The ability to generate substantial realized losses — in up, down, or sideways markets — is the whole point. For someone sitting on a $2–5M+ concentrated gain, this is often the highest-value tax tool available.

Key limitations: Leverage creates more "tracking error" (how much differs from the target index like SP500). More leverage = more tax alpha = more tracking error (which can be positive or negative). Best suited for large positions where the tax benefit clearly exceeds the fee and risk premium. The strategy can be de-leveraged to a point (i.e. 115/15), but exiting back to no leverage typically requires selling and realizing capital losses (ideally timed in lower-income years or a new state with low/no taxes).

Works for private stock? Mostly yes — with advance planning. You can run the long/short strategy on your non-concentrated portfolio assets while still holding private shares, using the generated losses to offset gains when you sell in a tender (as long as you have time, and capital).

Strategy 4: Exchange Funds

The closest thing to a "swap concentrated stock for a diversified portfolio without paying taxes" solution that actually exists. Also comes with real strings attached.

An exchange fund is a limited partnership where multiple investors, each with a different concentrated stock, pool their holdings together. You contribute your shares, and after a required holding period of 7 years, you receive back a diversified basket of stocks representing a slice of the whole pool.

No sale occurs at contribution. No capital gains tax at the time you contribute. Your original cost basis carries forward (deferred, not eliminated) and the tax only triggers when you eventually sell the diversified basket you receive back.

Diversification speed & completeness: Immediate and OK. Day one, your single stock is inside a diversified pool, typically of around 20-40 stocks and a required illiquid (typically real estate). Going from exposure of 1 stock to 30 is solid diversification, but its not the SP500.

Fees & cost: Moderate to high. Annual fees typically run 0.65% to 1.2%, and initial contribution fees may also exist.

Complexity: Moderate. You must be an accredited investor. The fund has to approve your specific security (not every stock is accepted). Annual K-1 reporting adds tax prep complexity. The legal partnership structure has nuances.

Control, flexibility & customization: Low. This is the least flexible structure in the toolkit. You contribute on a set date (whether you like the price of your stock that day or not), surrender control of the position for seven years, and cannot choose what ends up in your diversified basket you get back after 7 years.

Tax friendliness: Very friendly. No taxable event at contribution. And you get a diversified basket of stocks after 7 years.

Key limitations: The seven-year lockup is the big one. If you need liquidity, flexibility, or control within that window, this strategy will frustrate you.

Works for private stock? Mostly no. A handful of exchange funds do exist for pre-IPO stock holdings, but participating requires your company approval (and a lot don't allow it), which is a limiting factor.

Strategy 5: Section 351 ETF Conversion

The newest and least understood. Powerful, but only in the right circumstances.

A Section 351 exchange allows you to contribute a portfolio of stocks (not a single or couple) into a newly formed ETF, and receive ETF shares back at the same dollar value and the same cost basis, with no taxable event at contribution. The ETF's in-kind redemption mechanism then keeps it highly tax-efficient going forward.

Unlike an exchange fund, the ETF shares you receive back are liquid immediately. You can sell them anytime. The gain is deferred — not locked away.

Diversification speed & completeness: Immediate and full in terms of the contribution. Post-contribution, the ETF rebalances toward its target index. You're liquid day one, and can sell the ETF shares whenever you want.

Fees & cost: Lower than exchange funds over time. ETF expense ratios typically run 0.15–0.75% (you decide which ETF that is doing a 351 exchange to participate with, and accept that fee). No lockup, and no compounding partnership fee structure.

Complexity: Moderate to high. Requires coordination between your advisor, custodian, ETF sponsor, etc. Also typically a one-time event; typically can't be repeated on a rolling basis.

Control, flexibility & customization: Moderate. You contribute on a set date into an ETF that is starting up. You don't control the ETF's holdings; you just choose which ETF to do it with (i.e. the index/strategy you want for your investment). Once done, you control when to sell ETF shares. Better flexibility than an exchange fund; less than 130/30 or outright selling.

Tax friendliness: Very friendly. No taxable event at contribution. Gains deferred until you sell ETF shares.

Key limitations: Here's the critical one: this strategy cannot be used for a pure single-stock position. The IRS has a diversification test required for 351 exchanges. No single holding can exceed 25% of contributed value, and the top five holdings can't collectively exceed 50%.

Works for private stock? No. This requires publicly traded securities. It's a post-IPO strategy.

These Strategies Can Be Stacked

One thing worth emphasizing: this isn't a one-choice menu. The most effective plans for large concentrated positions often layer two or three of these together.

Some examples of how that works in practice:

Sell some outright + tax-aware long/short: Use the long/short to generate losses in the year you sold some outright. With good planning, can create no tax bill and a lot more diversification.

Long/short + staged selling: Run a 130/30 or 200/100 strategy alongside a multi-year selling plan. The loss engine offsets each tranche as you go. Very effective for large positions.

Exchange fund + sell the rest: Contribute a portion to an exchange fund for the long-term (assets you don't anticipate needing for a long time), then sell the remainder and use direct indexing or long/short to manage that tax.

351 exchange + long/short: Contribute a diversified slice into a 351 exchange at ETF launch, then use long/short harvesting to offset gains when you eventually sell ETF shares.

The combination that's right depends on your gain size, your state tax situation, your liquidity needs, your timeline, and frankly your psychological comfort with complexity. There's no universal answer — which is exactly why this article exists.

How to Actually Think About This

The framework I use with clients always prioritizes in this order:

Your life and financial goals first. What do you actually need this money to do? If you need cash in the next 12–18 months, a seven-year lockup is immediately irrelevant. If you're in a state with high capital gains tax and plan to move in two years, deferral becomes much more valuable. Life context shapes the strategy.

Portfolio risk second. A concentrated position isn't a tax problem — it's a risk problem that has tax implications. Most of the strategies above solve both. But never let saving on taxes create too high of risk in your portfolio (way too much pain/loss can occur if you do).

Tax optimization last, but DON'T skip it. Every dollar you defer or reduce on taxes can compound meaningfully over time. I've written before that tax deferral can be worth 2–5% per year in after-tax wealth. That's real. It just has to be evaluated against the cost, complexity, and loss of flexibility that each strategy requires.

The right answer for most people isn't the most sophisticated strategy. It's the most appropriate one — the one that actually fits your situation and that you'll execute consistently.

If you're not sure where to start, the cleanest diagnostic question is: What's the one thing you're most trying to solve for — speed, taxes, or flexibility? Your answer to that usually directs you toward the right starting point pretty clearly.

Have a concentrated position you're figuring out? I'd be happy to walk through the options with you.