Part 3 of 10 — SpaceX Equity Decision System

The Cost of Inaction: What “Wait and See” Can Really Cost You

Why "wait and see" isn't a neutral position — what delay actually costs in taxes, concentration risk, and lost optionality, and how to tell when waiting has crossed into an expensive non-decision.

What does delay actually cost SpaceX employees — specifically in taxes, concentration risk, and lost optionality?

Why do smart, analytical people still fall into "wait and see" even when they know better?

When is waiting actually the right strategic call — and when has it become a costly default?

What are the clear signals that inaction has crossed from strategy to mistake?

"Wait and see" feels safe. It requires nothing of you today. It keeps all your options open — or so it feels.

But here's the thing: waiting is a decision. It's just a passive one. And passive decisions around a SpaceX IPO carry their own very real costs — costs that don't announce themselves with a warning, but quietly compound in the background until suddenly they're expensive problems rather than manageable ones.

In my experience advising on more than $500 million in equity compensation, the most common expensive mistake I see isn't a bad tax decision or a poorly timed sale. It's doing nothing — because you didn't know what to do, or it felt too complicated, or you didn't want to pay for help (yet), or because SpaceX has gone up so consistently that inaction always seemed to work out fine.

That last part is worth sitting with. SpaceX's equity has been extraordinary. The stock has done nothing but increase in value for years. So if you've been doing nothing and it's been working, your brain has been rewarded for inaction — which makes it feel even more like the right default. That's how behavioral traps work. They feel like wisdom right up until they don't.

This article is about understanding what inaction actually costs — not to scare you into decisions you shouldn't make, but because making an active, informed choice to wait is very different from drifting into inaction by default.

Why Smart SpaceX Employees Still Fall Into "Wait and See"

Before we talk about cost, let's be honest about cause. The people who end up in "wait and see" mode aren't uninformed or careless. They're often engineers and scientists — analytical, thoughtful people who are very good at evaluating complex tradeoffs.

So why does inaction happen anyway? A few reasons, and they're worth naming because recognizing them is the first step to overcoming them.

The endowment effect. You've been inside SpaceX. You helped build it. Your equity isn't just a financial asset — it's tied to years of your life, late nights, launches, and mission. Selling feels like you're putting a price tag on all of that and walking away. That emotional attachment is real, and it's human. But it's also a bias — and it causes people to hold assets longer than rational financial analysis would support.

The anchoring effect. SpaceX has gone up. A lot. And every time you've thought "maybe I should sell some," the stock went higher and you felt vindicated for waiting. That pattern creates a powerful mental anchor: waiting has worked, so waiting is smart. The problem is that past performance of a pre-IPO company in a bull market for private tech is not a reliable indicator of what a newly public company will do once institutional investors reprice it against market expectations every single day.

Tax aversion. The capital gains bill on SpaceX shares is real — and likely very large. And there's something deeply frustrating about working for years, building meaningful wealth, and then immediately handing a significant portion of it to the government. I get it. But I've watched people hold through a 50%+ decline in company stock to defer a 24% capital gains rate. The math on that is not good.

Complexity paralysis. Between ISOs, NSOs, RSUs, ESPP, AMT, qualifying dispositions, blackout periods, and the SpaceX-specific tainting rule — the decisions are genuinely complex. And when something feels overwhelmingly complex, the brain's default is to postpone. "I'll figure it out when I have more information" is a reasonable-sounding response that often translates to "I won't figure it out until it's urgent."

None of this is a character flaw. All of it is predictable human behavior under conditions of uncertainty and complexity. But understanding why smart people wait helps you catch yourself doing it.

What Delay Actually Costs: Three Specific Price Tags

"Wait and see" isn't a free option. Here's what it costs.

Cost #1: Taxes — The Bill That Grows With the Stock

Every dollar of (hopefully) appreciation on your SpaceX shares between now and when you eventually sell is a dollar that will be taxed — at your applicable rate, in your applicable state, in whatever year you sell it.

If SpaceX appreciates between now and when you finally get around to selling, you're paying income and/or AMT taxes on a larger amount. That's not inherently bad — more gain is more money even after tax. But delay also creates a concentration of taxable events in a short window, which has its own cost.

Here's the specific version that hurts: imagine you exercise ISOs in the IPO year, start the qualifying disposition clock, and plan to sell at lockup expiration or beyond. But you haven't modeled the AMT. Or you've been telling yourself you'll think about it "closer to the IPO." Now the IPO is here, the lockup has expired, and your first open window is closing in three weeks — and you still don't have a tax plan. So you either sell reactively, potentially triggering a disqualifying disposition or selling the wrong lots — or you don't sell, stay concentrated, and wait for the next window.

The cost of that delay isn't just the tax you pay. It's the tax you pay on a worse set of facts because the planning didn't happen in time to create better options.

The other version: you know you have an AMT credit carryforward from a prior year ISO exercise. Selling qualifying ISO shares in the right tax year would help you recoup a meaningful portion of that credit. But if you wait until the wrong year — or until you've already sold different shares first — that recoupment opportunity may be reduced or lost. AMT credit recovery is time-sensitive. Waiting costs it.

Cost #2: Concentration — The Risk That Compounds Silently

Here's a number worth sitting with: according to research ~96% of individual U.S. stocks over long time periods have delivered no economic value (they matched or underperformed risk-free US Treasury bills as a group). The entire net wealth creation of the U.S. stock market has been driven by a very small number of extraordinary outliers.

SpaceX may be one of those outliers. I genuinely believe it has exceptional business fundamentals. But it's now valued that way ($1.25 trillion). And "may be" is doing a lot of work in that sentence — and the statistical reality is that most companies that looked exceptional at IPO were not, in fact, exceptional in the five years that followed.

More relevant for you specifically: the concentration risk isn't just about the stock price. It's about everything stacked on top of that single position.

When most of your net worth is in SpaceX, your concentration risk includes:

Vested shares and exercised options — what you own today

Unvested grants still coming — your future compensation is also SpaceX

Career exposure — your income, your professional network, your ability to get your next job — all partially tied to SpaceX's trajectory and reputation

That's not a concentrated stock position. That's a concentrated life position. And while SpaceX has been exceptional, that level of single-entity exposure is statistically a challenging path regardless of which company is at the center of it.

Every month you hold without a plan to diversify is a month you're adding to that exposure — not reducing it.

Cost #3: Optionality — The Flexibility You Don't Realize You're Spending

This is the one most people don't think about, and it may be the most insidious cost of all.

The decisions you can make before the IPO are different from — and in some cases significantly better than — the decisions you can make after it. The same is true of pre-lockup versus post-lockup. Every stage of the IPO process that passes without planning reduces the set of options available to you going forward. Concrete examples:

ISO exercise timing. Before the IPO, you have the ability to exercise ISOs at pre-IPO valuations — starting the qualifying disposition clock at a lower AMT bargain element. After the IPO at (let's assume) a $1.5 trillion valuation, the same exercise may trigger a substantially larger AMT bill. The option to act at lower cost exists now. It won't exist in the same form later.

Tax-year alignment. As I mentioned in the prior article (IPO Timeline Reality), a June 2026 IPO with 180-day lockup creates a rare scenario where both ISO exercises and qualifying ISO sales could potentially occur within the same 2026 tax year — creating AMT offset opportunities that don't exist if the two events fall in separate years. While you could do this in 2027, it's trickier, and valuations could be much higher (or lower).

Cash for life goals. If you need cash for a home purchase, a career transition, starting a company, or any other major life move in 2026–2027, your ability to fund those goals from SpaceX equity depends on having a plan in place before the liquidity windows open. Without a plan, you'll make those funding decisions reactively — often selling from the wrong lots at the wrong time, under personal financial pressure that clouds judgment.

The 60-day post-termination window. If you're considering leaving SpaceX at any point around the IPO, your window to exercise vested options is 60 days from your last day. That window doesn't pause while you figure out what to do. If you haven't modeled the exercise-vs.-walk-away decision in advance, you will be making it under time pressure, with limited information, while also managing a job transition. That is not the environment for good financial decisions.

When Waiting Is Actually the Right Call

I want to be clear: this article is not an argument that everyone should sell everything immediately. Waiting is a strategy I frequently use with clients. It just needs to be intentionally selected vs. an "I didnt know what to do so I didnt do anything" default. Here's a handful of situations where it's been the right move (and intentional):

When the tax math favors it. If you have RSU shares that are 10 months old, waiting 2 more months to clear the one-year mark converts short-term gains to long-term — worth doing. If you have ISO lots that are 11 months into the qualifying disposition period, waiting a month to clear the two-year grant requirement is worth doing. Strategic waiting for well-defined tax milestones is smart planning, not avoidance.

When you have a written plan and you're following it. If you've thought through your goals, built a sell schedule, and are deliberately executing a long-term plan — that's not "wait and see." That's disciplined execution. The distinction matters enormously: passive avoidance feels the same in the moment as intentional patience, but they lead to very different outcomes.

When your financial situation doesn't require de-risking. If you have substantial assets outside (inclusive or exclusive of SpaceX) and your financial plan allows you to take a ton of risk — then you can do so if you want (and a topic for a future article in this series). The urgency of diversification typically scales with concentration level (30% in one stock is a very different situation from 90%) and/or financial need (if you can live off $4 million for the rest of your life, you have very different choices if your stock is worth $5m vs. $25m)

When you're inside a blackout or lockup. You can't sell anyway. Use that time to plan — that's what it's for.

The Test: Is Your Waiting Smart or Expensive?

Here's a simple framework I use with clients. Answer these honestly:

1. Can you articulate in writing why you're waiting? "I want to see where the stock opens" is not a reason. "I'm waiting 47 days for this ISO lot to hit the one-year exercise anniversary" is a reason.

2. Have you modeled the downside? What happens to your financial plan if SpaceX trades 40% below the IPO price within 18 months? Can you fund your life goals from there? Have you actually stress-tested this, or are you only running upside scenarios?

3. Do you have a specific trigger that will cause you to act? "I'll sell when the time feels right" is not a trigger. "I'll sell 25% of my RSU shares in the first open window post-lockup regardless of price" is a trigger.

4. Are you waiting because of a genuine financial reason — or because the decision feels hard? This is the honest one. If the answer is the latter, that's not a strategy. It's avoidance.

If you can answer yes to 1, 2, and 3 with specific, concrete answers — you're waiting strategically. If you can't — you're doing "wait and see," and it has a cost.

The Most Expensive Non-Decision I've Seen

I'll leave you with a pattern I personally watched play out with a handful of friends and former colleagues.

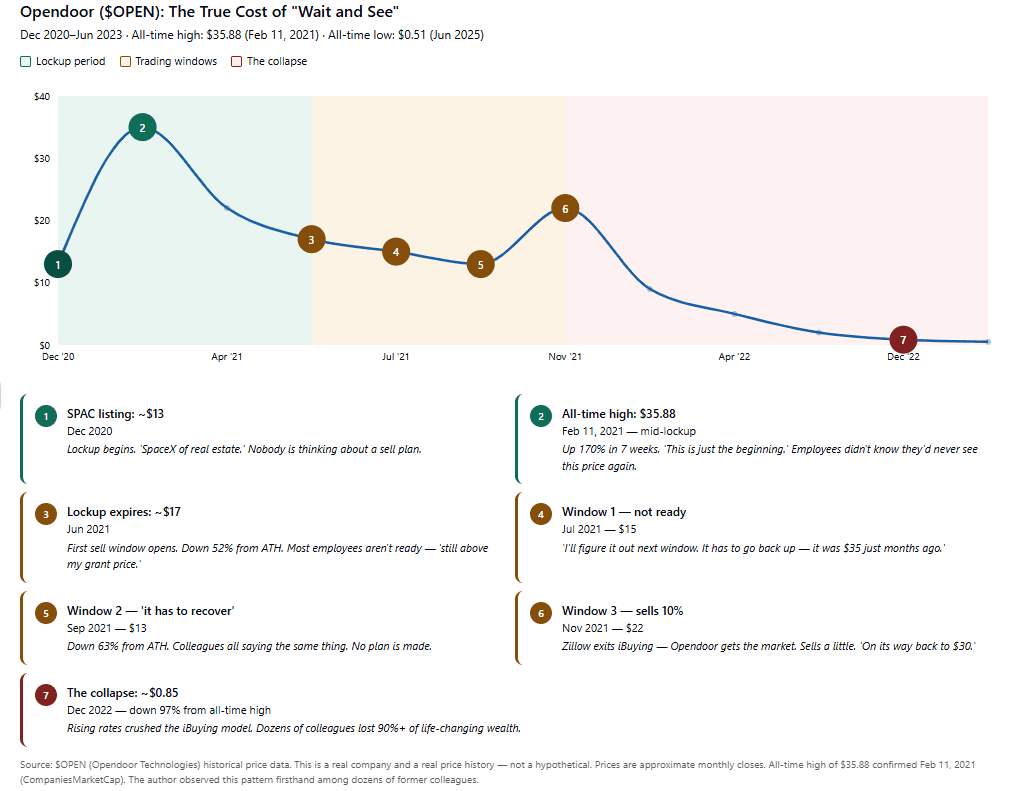

Employee has significant equity at a company approaching IPO. They plan to "figure out the plan" after the lockup expires. Stock looks really great during first half of the lockup (scales from $12 to a peak of $35), then declines to $17 by the time the lockup eds. When the window opened, they weren't ready to decide, and colleagues were all saying "it has to go back up, it was worth $30 just a month ago". Second window comes — stock is down to $14 and now selling feels even harder ("it has to recover"). Third window — stock is doing well, a competitor is struggling, they actually did get the stock rebound to $22. They sell a bit (finally), but not much because now "it feels like its on its way to that $30 target." Next 18 months: steady downward progress to below $1.00.

That isn't hypothetical. It was my former employer ($OPEN) — and I watched dozens of former colleagues lose 90%-plus of their wealth due to inaction or unreasonableness.

Challenge is the story repeats frequently with with smart, successful people at many other companies. The mechanism is always the same: no plan made in advance means every window becomes a new decision under new emotional pressure, and those decisions get progressively harder to make.

The SpaceX IPO is one of the largest wealth events in the history of the technology industry. The people who navigate it with the most confidence and least regret will be the ones who made thoughtful and well researched decisions before the pressure arrived — not after.

If this applies to you, the decisions are worth getting right.

If you're a SpaceX employee approaching liquidity, the sequencing, timing, and structure of just a few decisions can materially change your long-term outcome.

I work with a limited number of clients each year to help navigate these exact decisions before and after liquidity events.

Last updated: April 8, 2026

← Back to SpaceX hub