Part 7 of 10 — SpaceX Equity Decision System

ISOs and AMT: Estimate It Before You Trigger It—Then Reduce and Recover It

The AMT mechanics, dual-basis math, and multi-year credit recovery details every SpaceX employee with ISOs needs to understand before — not after — they exercise

This article picks up directly from Article 6 on Exercise Strategy. If Article 6 was about whether and when to exercise, this is about what happens to your tax bill when you do — and how to manage it.

How does AMT actually get triggered when I exercise ISOs?

What is "dual basis," and why does it matter more than almost any other tax concept for SpaceX ISO holders?

Which levers can I still pull to reduce my AMT exposure?

What does AMT credit recovery actually look like, year by year, in real dollars?

The Tax That Surprises People — and the One They Forget Comes Back

I've sat across from clients who exercised ISOs in good faith, didn't fully understand AMT, and got blindsided by a tax bill in April that was multiples of what they expected. I've also guided clients through an ISO exercise with AMT, paid a large bill, and then strategically recouped a meaningful portion of it over the following years — exactly as the system is designed to allow.

The difference between those two outcomes isn't intelligence. It isn't even tax sophistication, really. It's whether someone took thirty minutes — before exercising — to understand two things:

How AMT gets triggered, and how to estimate it

How the AMT credit comes back, and what makes that recovery faster or slower

That's what this article is about. We'll use the same worked example from Article 6 — 4,000 ISOs, $56 strike, $526 fair market value at exercise — so the math carries through cleanly. By the end, you'll have a directional picture of what AMT looks like for that position, what levers you have to manage it, and what the recovery timeline actually looks like.

This is not a substitute for running the numbers with your advisor. Your specific situation — income, state of residence, deductions, capital gains, other AMT preference items — changes the math. But you should walk into that conversation with a working framework, not a blank stare.

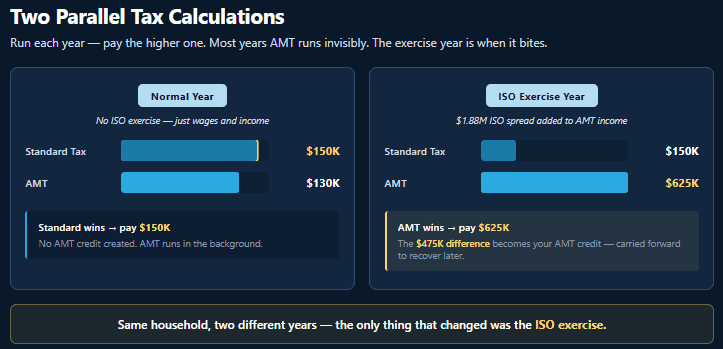

Step 1 — Understand That You Live in Two Tax Systems

Most people think of taxes as one calculation. They're not. The U.S. tax code runs two parallel systems: regular tax and the Alternative Minimum Tax. You pay whichever one comes out higher.

In most years, regular tax is higher, and AMT is invisible to you. It's running in the background, but it never wins.

The year you exercise a large ISO position is the year AMT often wins — and it can win by a lot.

Here's why: You've heard that ISOs have "favorable tax treatment." The reason for that is the regular tax system doesn't recognize the spread on an ISO exercise as income (assuming you don't sell the shares in the same year — that's the qualifying disposition path from Article 6). But the AMT system does recognize the spread as income.

So in the year you exercise:

Regular taxable income looks roughly normal.

AMT income spikes by the full spread.

If that AMT income is large enough to push your AMT calculation above your regular tax calculation, AMT wins — and you owe the difference.

For SpaceX employees with concentrated ISO positions, that difference can easily run into the high-six, or seven, figures.

Step 2 — Estimate It Before You Trigger It

Let's run the math on the worked example from Article 6:

4,000 ISOs

Strike: $56/share

FMV at exercise: $526/share

Spread (the AMT preference item): $470 × 4,000 =

$1,880,000

That $1.88M spread is added to your AMT income in the year of exercise.

For a married SpaceX household already earning, say, $400K–$600K in W-2 income (which includes RSU vesting), the AMT calculation in that year can produce a federal AMT liability in the neighborhood of $500,000 — give or take, depending on state, deductions, and how the exemption phase-out hits at that income level.

That is a real number. It is due in April. And critically — if your plan is to hold those shares for a qualifying disposition — you cannot sell the shares for a year after exercise. Which means depending on when you exercised, you may need to fund your AMT bill from outside cash.

The single most important thing you can do before exercising any meaningful ISO position is to model the AMT bill with your advisor, on your specific numbers, before pulling the trigger. Not after. Not at year-end. Before.

If you don't have an advisor who can model AMT for an equity-heavy SpaceX household, that's a gap you should close before exercise — not the week the tax bill arrives.

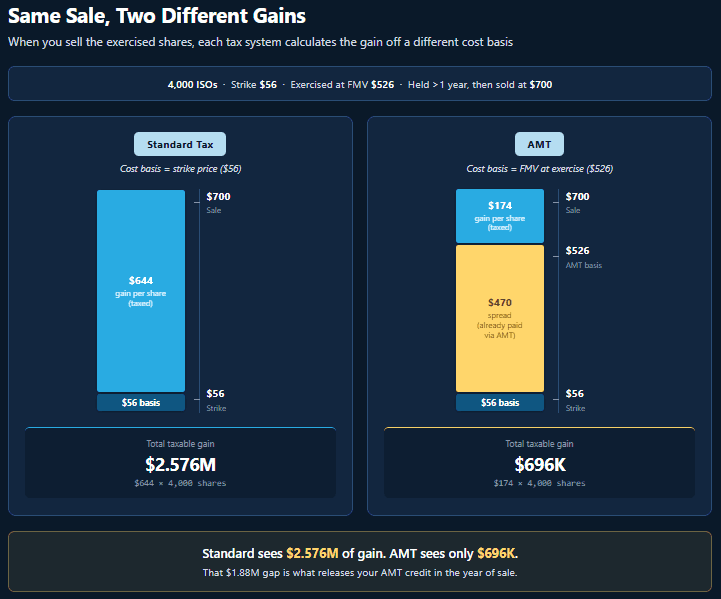

Step 3 — The Dual Basis Concept (This Is the Key Unlock)

This is the part most ISO articles either skip or bury. Don't skip it. Dual basis is the conceptual key that explains why AMT isn't a permanent loss — it's a timing mechanism.

When you exercise ISOs and hold the shares, you now own shares with two different cost bases simultaneously:

Regular tax basis: $56/share: (your strike price — what you actually paid)

AMT basis: $526/share: (the FMV on exercise day — because AMT already taxed you on the spread)

You read that right. The same share has two different cost bases at the same time. One under each tax system.

Why does this matter? Because when you eventually sell those shares, the two systems calculate your gain differently.

Say SpaceX is at $700/share when you sell, and you've held long enough for a qualifying disposition (more than 2 years from grant and more than 1 year from exercise):

Under regular tax: Your gain is $700 − $56 = $644/share of long-term capital gain

Under AMT: Your gain is $700 − $526 = $174/share

That gap — $470/share, the original spread — is enormous.

In the year of sale, your regular tax on the gain will be much larger than your AMT on the gain. Regular tax wins that year by a wide margin. And here's the magic of the system: when regular tax exceeds AMT, your prior AMT credit gets released to offset the regular tax bill. That's how you get the AMT back.

The dual basis isn't a quirk. It's the mechanism. The IRS's parallel-systems design assumes you'll eventually sell, the gap will reverse, and the credit will flow back to you. Your job is to understand the timing of that flow — and plan the rest of your finances around it.

Step 4 — The Levers You Have

Here's the honest update: a few years ago the most powerful lever for managing AMT on a SpaceX position was the AMT free window — exercising small chunks of ISOs each year while the spread was still modest. Calculated correctly, you could exercise a decent bit of ISOs without triggering AMT.

That door is now technically still open (after SpaceX un-pauses the current hold to launch its IPO), but the massive appreciation in SpaceX shares has resulted in amount of "AMT free" exercises most employees can do being a very small number of ISOs, rendering that strategy mostly moot. That leaves:

Lever 1 — Spread exercises across tax years. You have flexibility on which shares to exercise when, and can spread an exercise across two or three calendar years to keep the spread in any single year smaller. The math gets dramatically less painful when $1.88M of preference becomes $625K per year over three years instead of $1.88M in one. (Note: this only works if the price doesn't run away from you. The trade-off is locking in a known spread today vs. a possibly larger spread tomorrow.)

Lever 2 — Coordinate with your income years. The "AMT free" window in normal years isnt that great. But due to the way AMT vs. standard tax work, both (i) lower-income years (sabbatical, career transition, gap year, spouse out of the workforce) and (ii) higher income years (heavy RSU vesting; NSO exercises; ISO disqualifying dispositions) can give you a lot more room.

Lever 3 — Pair ISO exercises with AMT recoup. Strategy one above suggested spreading your AMT bill across years to make it less painful. To amplify that, you can create a paired strategy of selling the shares from prior ISO exercises in the same year. Those share sales recoup paid AMT, which will further lower your AMT bill.

Lever 4 — Intentionally trigger a disqualifying disposition. Optimizing ISOs and AMT can be worthwhile, with tax rate reductions of as much as 17%. But, it has risks. If you're not able to recoup paid AMT (i.e. leaving the state of CA), or if the price declines from exercise to sale it makes federal AMT recoup much harder. Sometimes it isn't worth it, and you just want to conduct a cashless exercise, pay the tax, and move on.

None of these are decisions to make solo. Every one of them gets sharper with an advisor running the actual numbers. But knowing which levers exist — and which one fits your situation — is what makes that conversation productive.

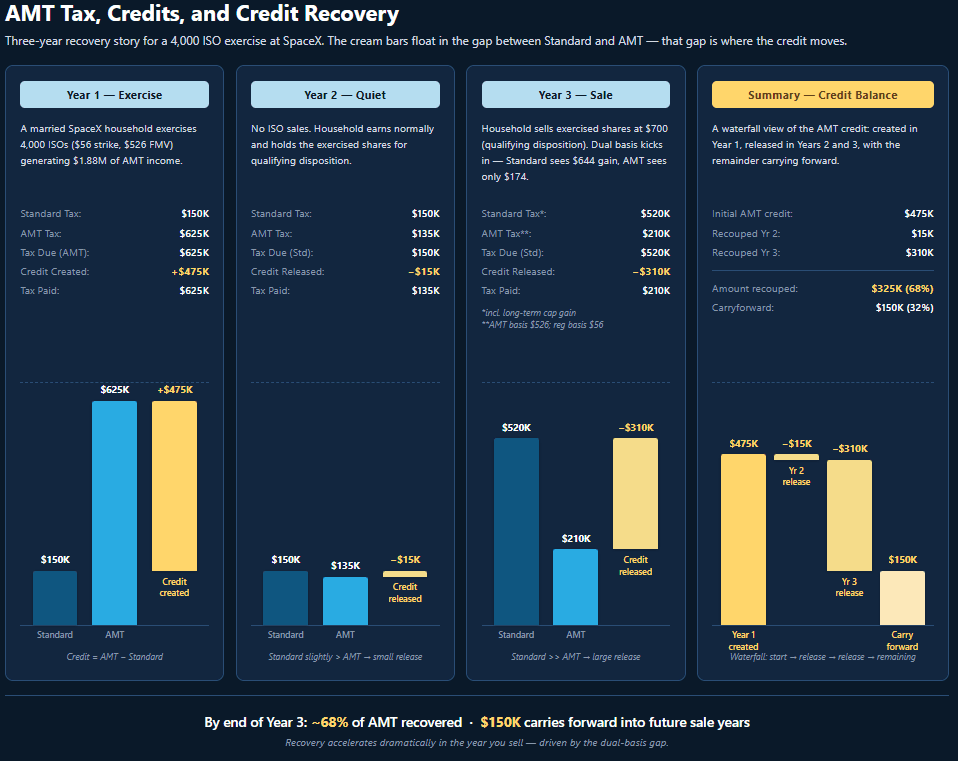

Step 5 — The 3+ Year AMT Credit Recovery Story

This is the part that turns AMT from intimidating into manageable: recouping the AMT you've paid. Here's how it works, using a household with the kind of profile we've been working with (assume they do not live in a state like CA that also has its own AMT):

Year 1 — The Exercise Year. You exercise the 4,000 ISOs. Spread is $1.88M. AMT calculation comes in at roughly $475K higher than regular tax. You write a check for the AMT difference. Your AMT credit balance: ~$475K, carrying forward.

Year 2 — The "Quiet" Year (No ISO sales). You don't sell any of the exercised shares yet — you're holding for qualifying disposition. Your regular tax that year exceeds your AMT (because there's no spread feeding the AMT calculation). The system releases a portion of your AMT credit against the regular tax bill. Modest release — maybe $10K–$20K — but it's something at least.

Year 3 — The Sale Year. You sell a portion of the exercised shares. Qualifying disposition rules apply, so the entire gain is long-term capital gain at the regular tax level. But here's where dual basis kicks in: under regular tax, the gain is enormous ($644/share). Under AMT, the gain is much smaller ($174/share). Regular tax for the year is now far larger than AMT — and a substantial chunk of your remaining AMT credit gets released against that regular tax bill.

In a real client scenario from our practice — different share counts and prices than the SpaceX example, but the same structural mechanics — a married household that paid roughly $600K in AMT in Year 1 had recouped about 68% of it by the end of Year 3. The remaining ~32% continued to carry forward and will release in future sale years.

The takeaway: AMT is a real cost. It is not a permanent loss. The credit recovery is real, it's significant, and it accelerates dramatically in the year you sell. But it requires that you (a) hold long enough for a qualifying disposition, (b) actually sell shares to release the credit, and (c) have a CPA tracking the dual basis correctly across multiple tax years. If the basis isn't being tracked, the credit doesn't release on schedule.

A Specific Risk Worth Naming: AMT Credit Recoup is a LOT Header if the Price Declines

Everything we just walked through — the dual basis, the 3+ year recovery, the (estimated) 68% recoupment — assumes one thing: the price is the same or higher when you sell than when you exercised. That's what creates the regular-tax-greater-than-AMT gap that releases the credit. If the price doesn't cooperate, the recovery story breaks down fast.

There is a weird tax quirk when you have a capital loss; you can only utilize $3000 of it each year and the rest roles forward. That rule applies on the AMT side of your taxes as well.

Walk through the same worked example, but assume SpaceX is trading at $400 when you sell instead of $700:

Regular gain: $400 − $56 = $344/share (still positive, but $300/share less than the $700 scenario).

AMT gain: $400 − $526 = −$126/share (a loss under the AMT system, because you're selling below your AMT basis).

The AMT credit release in the year of sale is now driven by a much smaller regular gain and an AMT loss that is capped at $3000 per year (the rest rolls forward). Both of those items notably reduce the size of AMT credit recoup you can realize in this year, pushing more of the credit into the future.

The math gets worse the lower the price goes. At a sale price below your strike — meaning the shares are underwater entirely — the credit is essentially trapped. It carries forward indefinitely on Form 8801, but it has nothing to release against except other future capital gains if you ever have them.

This is what I mean when I tell clients ISOs and AMT aren't always a sure thing. The credit can be recouped; but it's not guaranteed. And the variable that determines whether it does — the future stock price — is something none of us controls.

A few related risks worth flagging in the same breath:

State residency change. Federal AMT credit follows you across state lines. State-level AMT credits (California's, in particular) generally do not. If you exercise in California, pay California AMT, and then move to Texas before selling, the federal credit recovers normally — but the California credit may not be recoverable at all. For SpaceX employees considering a post-IPO move, this is worth modeling before the move, not after.

Income disappearance. AMT credits release against regular tax liability. If your post-IPO life involves drastically less income due to a sabbatical, early retirement, or similar— the credit recovery likely slows down. This isn't catastrophic (the credit still carries forward), but it stretches the timeline meaningfully.

Concentration on top of trapped credit. The worst-case version of this risk is holding a large concentrated SpaceX position and a large unrecovered AMT credit. If the stock declines, you're losing wealth on two fronts simultaneously: the position itself, and the credit you can no longer recoup or will take many more years to do so. This is part of why Article 4's diversification logic and Article 5's holding discipline matter so much. The exercise decision doesn't sit in isolation — it interacts with everything else in your plan.

One Question I Ask Every Client Before They Exercise ISOs

"If we model the AMT bill at your specific numbers, run a dual-basis projection of the credit recovery over three years, and stress-test what happens if SpaceX drops 40% between exercise and sale — do you still want to do this?"

If the answer is yes after that exercise, you're making a real decision. If the answer wavers, the answer is to wait, exercise less, do some via cashless exerciser/disqualifying disposition, or restructure the timing.

The clients who get this right aren't smarter than everyone else. They just refuse to exercise into uncertainty without modeling the downside first.

To Recap

Estimate before you trigger. Model AMT with your advisor on your actual numbers — not a generic calculator — before pulling the trigger.

Understand dual basis. Same share, two cost bases. The gap between them is what releases the AMT credit when you eventually sell. It's the conceptual key to everything.

Strategically decide which levers/path is best for you. Spreading across years, sizing the exercise, coordinating with change of income years, or possibly not playing the game and just cashless exercising are your primary tools.

Plan the recovery. AMT credit recovery is real and significant — but it requires you to actually sell shares, hold for qualifying disposition, and have an advisor tracking dual basis across multiple tax years.

Be aware of an OK with the risk if the price declines. If you're not comfortable with "trapped" AMT credits, that's your sign that you need to reduce your plan.

AMT isn't the boogeyman it gets made out to be. But it's also not optional, and it's not forgiving when you exercise blind.

The clients who get this right run the math twice — once to estimate the bill, once to plan the recovery — before they pull the trigger. The clients who don't get it right almost always do, eventually. They just pay a much bigger tuition than they needed to.

If this applies to you, the decisions are worth getting right.

If you're a SpaceX employee approaching liquidity, the sequencing, timing, and structure of just a few decisions can materially change your long-term outcome.

I work with a limited number of clients each year to help navigate these exact decisions before and after liquidity events.

Last updated: May 4, 2026

← Back to SpaceX hub