On June 16th, SpaceX traded as high as $225. If you're a SpaceX employee, I'd bet that number is now living rent-free in your brain.

You watched your equity get marked to a figure, which for a moment was real. Then the stock slid. By this week it's back near $155 — down roughly 30% from that peak, even as it sits comfortably above the $135 IPO price.

And here's what I'm seeing already, in conversations with clients and connections inside the company: some are anchoring to $225. Seeing that price (briefly) in the market has convinced them it's worth that much, and now they're strongly considering selling less if the stock stays around ~$150.

I want to be blunt, because this is the kind of thing that quietly wrecks an otherwise great financial outcome: that $225 was never a real assessment of what SpaceX is worth. It was the output of a set of market mechanics so unusual that I'm not sure we've ever seen them stacked together like this in the history of public markets.

Let me show you what's actually setting the price, and why building your plan around any single number on the screen, high or low, is one of the riskiest things you can do right now.

First, the Boring Truth: This Is Just What IPOs Do

Before we get to what makes SpaceX weird, let's establish what's normal, because the bouncing-around part is completely normal. If you understand that, you stop panicking and you stop anchoring.

New stocks are violent. They spike on scarcity and hype, overshoot wildly, and then settle once supply catches up and the first real earnings reports force the market to price the business instead of the story. This happens almost every time. Two recent examples:

Figma. Priced at $33 last summer. It soared 250% to close at $115.50 on its very first day, then touched $142.92 the next session. Euphoria. Then reality. By late November it had fallen below its $33 IPO price, and today trades in the $20s, down more than 80% from its peak. An employee who mentally calibrated to the ~$140 stock price (which due to the lockup they could never sell at) is now far far worse off.

Cerebras. The AI chipmaker positioned as the closest thing to an Nvidia challenger. Priced at $185. Opened at $350, spiked to $385 intraday, and closed its first day at $311. As of today, its around $180 a share, below its IPO price.

These aren't obscure disasters. Other high profile tech companies like Circle and CoreWeave also peaked shortly after their IPO and then declined.

In plain English: an IPO spike is the anomaly; the price settling in weeks/months afterwards is the more reliable one.

So when SpaceX runs from $135 to $225 and back to $150s, the way to interpret that is: this is normal and what newly public stocks do. And the price that matters is the one we have today as it starts to settle, not the one we briefly saw.

SpaceX Also Isn't a Normal IPO (By a Long hot)

This is where SpaceX drastically departs from the standard IPO playbook. Most of the time, early post-IPO volatility is supply and demand finding each other. With SpaceX, there are four structural oddities affecting stock supply and demand (which determines price) in ways we've never seen before (and which have very little to do with whether the company is a good investment). It's important to understand them.

Driver #1: The Float Is VERY Low

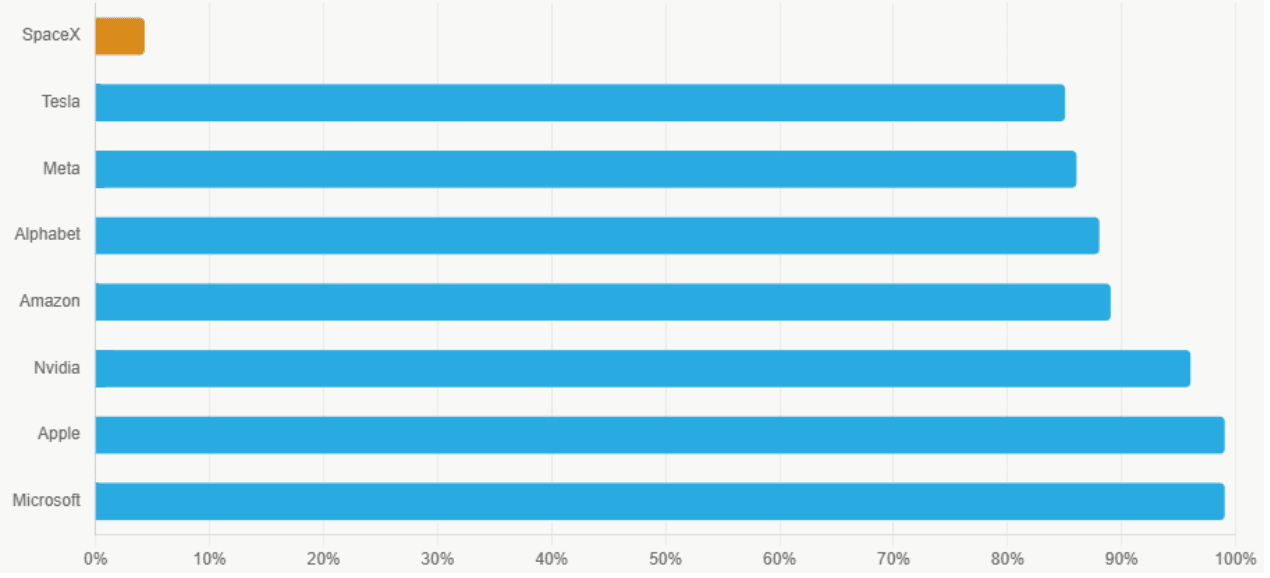

When SpaceX went public, it sold about 555 million shares against more than 13 billion shares outstanding, which calculates to a public float of roughly 4.25%. For context, mature companies in the major indexes typically trade with free floats above 80%. The market is pricing 100% of a $1.7-trillion-plus company off the trading of about 4% of its shares.

This matters -- a lot -- because the price of a stock is determined by supply (people who own and are able/willing to sell) and demand (people who want to buy). When a very small amount of shares freely trade, that can make supply and demand grossly out of whack and distort pricing (often inflating it).

When the float of shares for a publicly traded company is thin, which it is with SpaceX, weird things can happen. Price becomes more heavily influenced by supply and demand, and less so by the consensus opinion of company value.

If context is helpful: The so called "Magnificent 7" of Microsoft, Apple, Nvidia, Amazon, Alphabet/Google, Meta/Facebook, and Telsa all have more than 80% of shares freely floating.

Driver #2: Market Indexes Will Soon Be a Forced Buyer Who Doesn't Care About Price

Normally, everyone buying a stock is making an intentional buying choice. But not always. Indexes and the ETFs that track them are forced buyers.

Nasdaq, FTSE Russell and MSCI are all stock market index providers, and they changed their rules for how quickly a company like SpaceX can be included in the index. Nasdaq used to require a minimum of 3 months of "seasoning" in the market before a company could be included in one of its indexes. Now it's only 15 trading days (by early July).

Here's why that matters to the price. The moment SpaceX joins, every fund tracking the Nasdaq-100 is mandated to buy it to mirror the index — non-discretionary, price-agnostic demand. These funds don't have an opinion. They don't care if it's overvalued (or undervalued). The index has rules for what companies are included or not, and they follow the rules, so they buy, at whatever price the market is quoting. For context, BNP Paribas estimates Nasdaq-100 index inclusion alone could generate roughly $8 billion in forced passive buying, with total passive purchases potentially reaching $30 billion.

Driver #3: The Nine-Stage Lockup that Drip-Feeds Supply

Most IPOs run a simple 180-day lockup: insiders are frozen, then on one day the gate opens. Sometimes there is a second early release. But with SpaceX, it's a staggered structure with roughly nine separate release events between August and December 2026.

Similar to 1 and 2 above, it's an atypical market event that will have a significant impact on supply and demand (specifically supply for this driver).

Driver #4: The Supply Offset (More Supply Creates More Forced Buying Due to Index Rules)

Remember in #2 above where we talked about how Indexes are forced buyers? And we talked about how they have specified rules about what companies are included and how they calculate the percent of the index a company will be?

Well, some index providers base that (at least in part) off of float. Using the Nasdaq-100 again, for calculating how much of the index a company should be, they use the lesser of (i) shares outstanding or (ii) 3x free float.

Per above, SpaceX has very limited float, so Nasdaq's 3x free float rule determines SpaceX's percent inclusion in the index. But as the float increases (which will occur when lockup release dates pass), SpaceX's weighting will increase, creating more forced Nasdaq-100 index buying.

What Does All of This Mean for SPCX Shares?

In short, it means that SpaceX's share price is being impacted -- and will continue to be impacted over the coming months -- by a handful of factors that are quite atypical. Some spike demand, others spike supply.

How does this all play out over time? I have no idea...

Will the stock price go up or down from here? I have no idea...

Does SpaceX's stock price reflect the market's fair value estimate for the company? With most companies I'd answer "generally yes"; with SpaceX I'm not sure.

What Does All of This Mean for YOU?

Develop your own plan, and don't anchor to any price you see near-term (especially not the temporary $225 price spike). As I've written countless times in my 10-part SpaceX IPO planning series, you need to decide to sell (or not) based on your personal needs and risk tolerance.

Now that SpaceX is public, there is a lot of psychological whipsawing that may occur. I experienced it myself as an employee for 2 companies that IPO'd. And I also experienced too many colleagues anchoring to a post-IPO $30 price high they saw during the lockup, making them refuse to sell post-lockup when the price was ~$17 (and which eventually dipped below $1 per share).

Wall Street Analysts are arguing about a stock price, but YOU are making a decision about your net worth and financial future. Those are completely different scenarios. The analyst can be wrong and move on. You only get one chance to navigate this.

So flip the whole thing around. The right reference point was never the price. It's you:

What does this money actually need to do for your life, and on what timeline?

How concentrated is your net worth in a single, volatile, newly public stock?

What's your tax picture, and what does diversification cost or save you?

What plan can you commit to regardless of whether the stock is at $150 or $250 next quarter?

Build your plan around those answers (your financial profile, your goals, your risk), and the price on any given day becomes an input you act on, not a target you wait for.